Accounting,Business,Business Consultant,Corporations,Education,Forensic Accounting,Fraud & Criminal Investigations,Small Business

Occupational Fraud in 2026: What Organizations Continue to Get Wrong

Fraud has become more sophisticated, more expensive, and more difficult to detect—but many of the patterns behind occupational fraud remain surprisingly familiar. A major global review of more than 2,400 real fraud cases across 143 countries and territories offers an eye-opening look at how fraud occurs, who commits it, and which internal safeguards can make a measurable difference.

The findings paint a clear picture: fraud is not limited to large corporations, financial institutions, or headline-making scandals. It affects organizations of every size and industry. More importantly, many fraud schemes continue for months—or even years—before anyone notices.

The Cost of Fraud Remains Staggering

Organizations continue to experience significant financial damage from occupational fraud. Analysts estimate that businesses lose approximately 5% of annual revenue to fraud-related activity. Applied globally, that translates into trillions of dollars in potential losses each year.

Among the cases studied, the median financial loss reached six figures, while average losses exceeded one million dollars per case. Even more concerning, one out of every five cases resulted in losses exceeding $1 million.

Fraud is rarely a minor accounting issue. Beyond financial loss, organizations often face operational disruption, damaged trust, legal complications, and reputational harm.

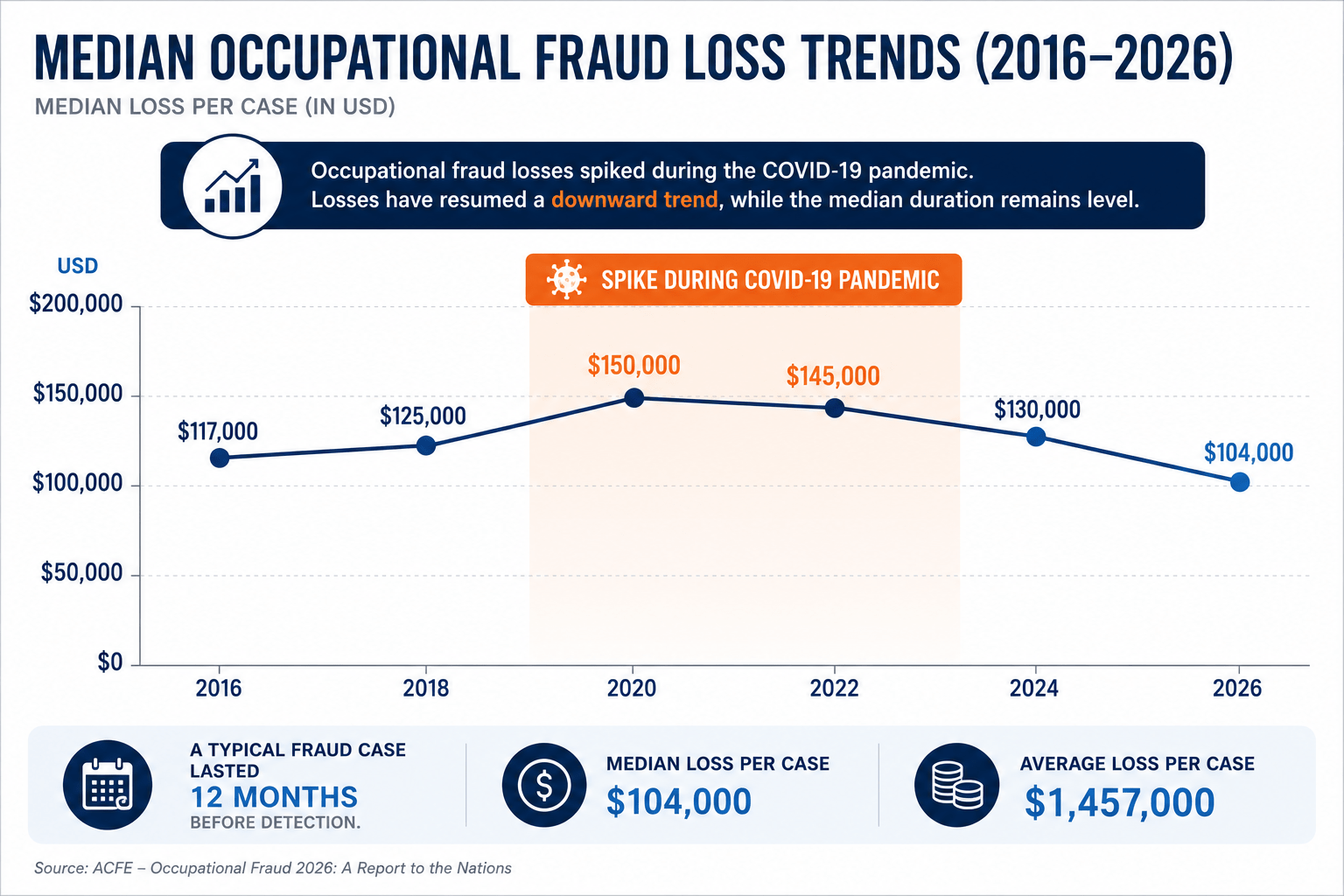

Fraud Often Lasts Longer Than People Realize

One of the more concerning findings is duration.

The typical fraud scheme lasted approximately one year before detection.

That means organizations are frequently absorbing financial losses for extended periods before a problem surfaces. Fraudsters often exploit familiarity, routine processes, and trust. Over time, repeated small actions can evolve into substantial losses.

The longer a scheme remains hidden, the greater the financial impact tends to become.

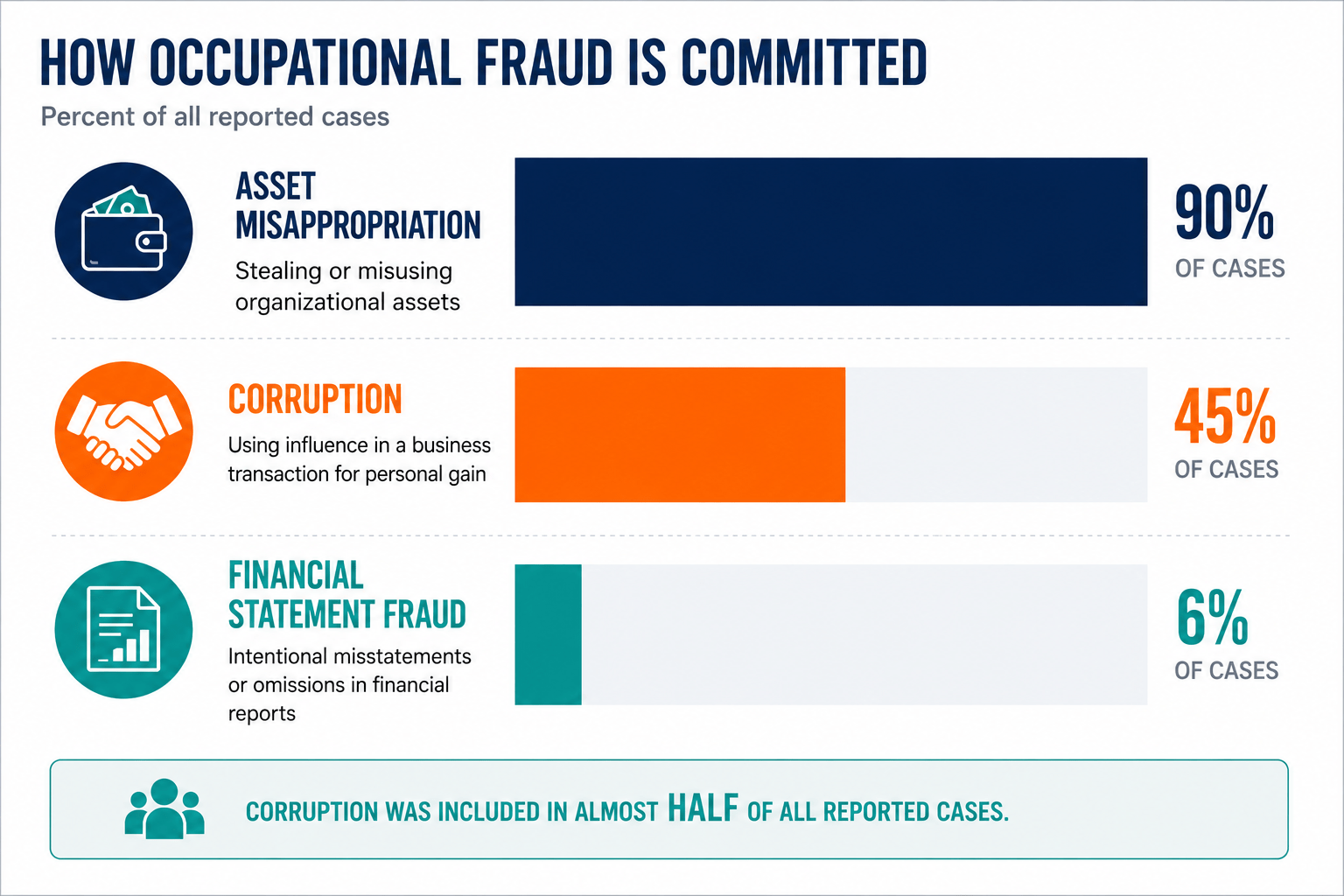

The Three Main Types of Occupational Fraud

Occupational fraud generally falls into three categories.

Asset Misappropriation

This remains the most common form of fraud and involves theft or misuse of company resources.

Examples include:

• Payroll schemes

• Expense reimbursement abuse

• Billing fraud

• Cash theft

• Inventory misuse

Although these schemes occur most frequently, they often generate lower median losses than other forms of fraud.

Corruption

Corruption continues to rise and now represents a significant percentage of reported fraud cases.

Examples include:

• Conflicts of interest

• Kickbacks

• Bribery arrangements

• Vendor manipulation

Corruption can be particularly difficult to identify because it often appears embedded within ordinary business relationships.

Financial Statement Fraud

This category occurred least frequently but produced the largest financial damage.

Financial statement fraud can include:

• Revenue manipulation

• Hidden liabilities

• Inflated assets

• Improper reporting

Cases involving manipulated financial reporting generated dramatically larger losses than other fraud categories.

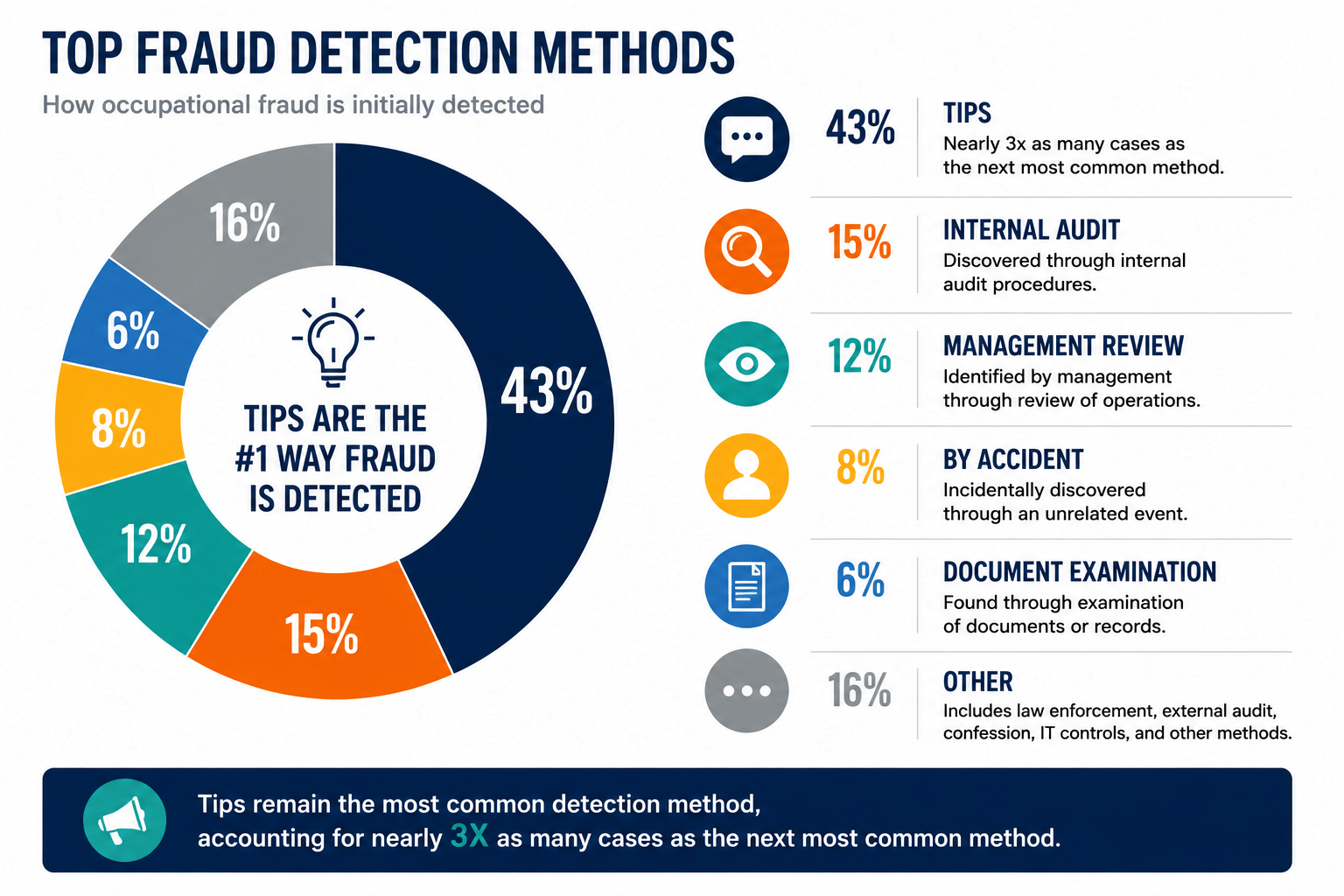

Tips Continue to Catch More Fraud Than Anything Else

Despite advances in technology and analytics, one finding has remained remarkably consistent over decades of fraud research:

People still uncover fraud more often than systems.

Whistleblower tips remained the leading method for detecting fraud.

Employees, managers, customers, vendors, and other individuals often notice unusual behavior long before automated systems identify irregularities.

This highlights an important reality: organizations can invest heavily in technology, but employees often remain the first line of defense.

Small Organizations Continue to Face Greater Risk

Smaller organizations remain especially vulnerable.

Large organizations frequently have:

• Dedicated accounting teams

• Segregation of duties

• Formal approval systems

• Internal audit departments

• Established anti-fraud programs

Smaller businesses often rely on a limited number of trusted individuals who handle multiple financial responsibilities.

While trust is important, concentrated authority can create opportunities for misconduct if proper oversight does not exist.

Many fraud cases arise not because organizations lack honest employees, but because weaknesses in internal controls create opportunity.

Fraudsters Rarely Fit Stereotypes

One of the most interesting findings is that fraudsters frequently appear ordinary.

Most are not career criminals. Many have no prior fraud history and often hold positions of trust.

However, patterns continue to emerge.

Fraud losses generally increase when perpetrators:

• Hold higher organizational authority

• Have longer tenure

• Possess greater access to systems or funds

• Have decision-making power

As individuals move upward within organizations, their ability to bypass controls often increases.

Authority and trust can become significant risk factors when oversight weakens.

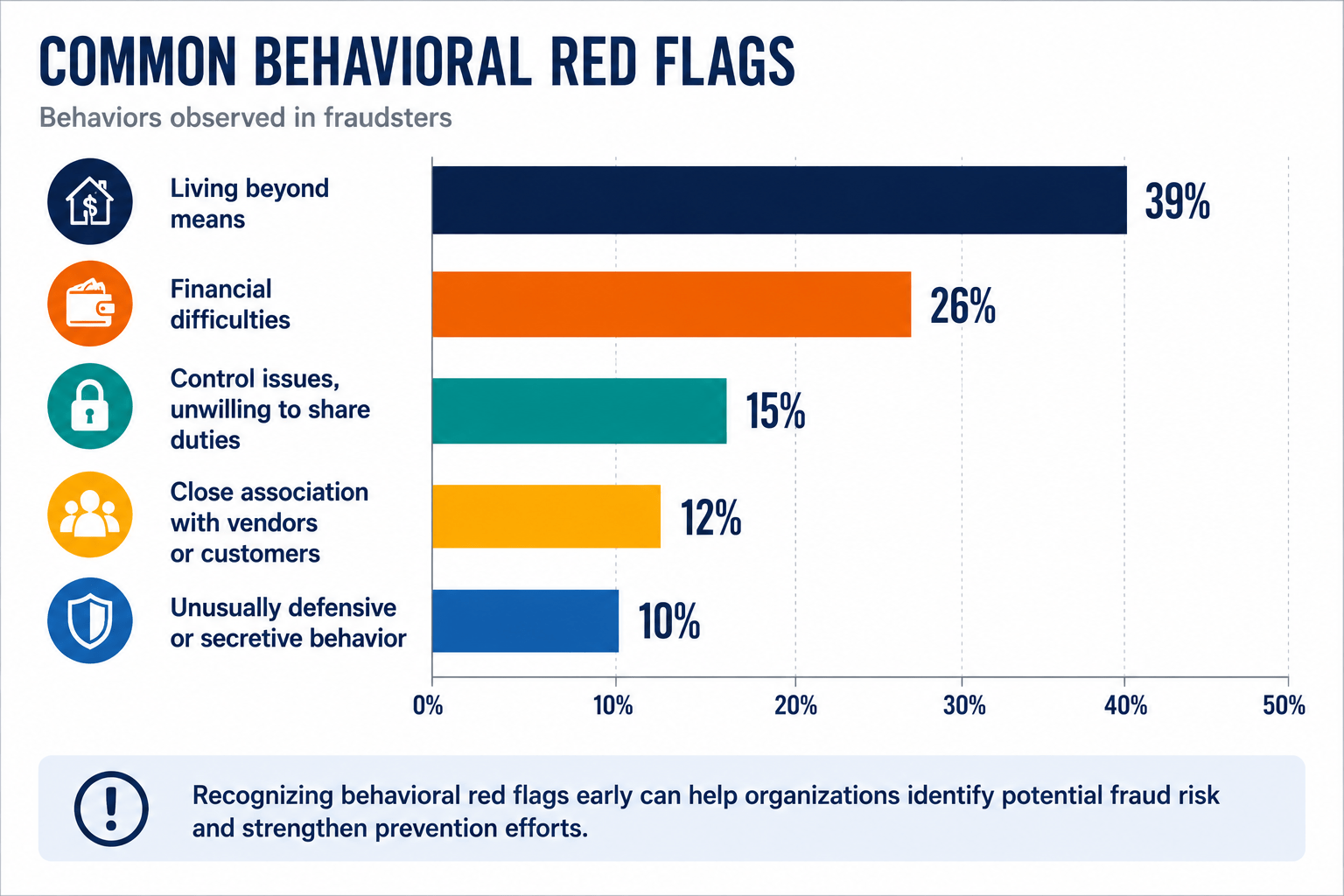

Behavioral Red Flags Often Appear Before Fraud Is Discovered

Most fraud cases involved observable behavioral warning signs.

Common red flags included:

• Living beyond apparent means

• Financial difficulties

• Unusually close vendor relationships

• Excessive control issues

• Reluctance to share duties

• Irritability or defensiveness

• Unexplained lifestyle changes

No single warning sign proves misconduct. However, patterns of behavior can provide valuable context when combined with other concerns.

Internal Controls Continue to Make a Difference

Organizations with stronger anti-fraud measures generally experienced lower losses and shorter fraud durations.

Certain controls repeatedly demonstrated measurable impact:

• Anonymous reporting systems

• Fraud awareness education

• Management review procedures

• Internal audits

• formal fraud risk assessments

• Data monitoring and analytics

Perhaps most importantly, organizations that actively discussed fraud awareness appeared better positioned to detect issues earlier.

Fraud prevention is not solely about accounting systems. Culture, communication, and transparency continue to play major roles.

The Bigger Lesson

Three decades of fraud research continue to reinforce one important reality: fraud evolves, but human behavior often does not.

Technology changes. Industries change. Economic conditions change.

Yet occupational fraud repeatedly follows familiar patterns involving opportunity, access, trust, and oversight.

Organizations cannot eliminate risk entirely. However, understanding how fraud commonly develops—and recognizing the warning signs early—can significantly reduce exposure.

Awareness remains one of the most valuable tools organizations possess.

![]()

Pivotal Forensic Accounting & Audits

contactus@pivotalaccountant.com

Phone: 253-752-3920