Accounting,Financial Crimes,Forensic Accounting,Fraud & Criminal Investigations,In the news,Litigation Support & Investigation

Inside the King County Regional Homelessness Authority (KCRHA) Audit: A Forensic Look at Missing Funds and Weak Controls

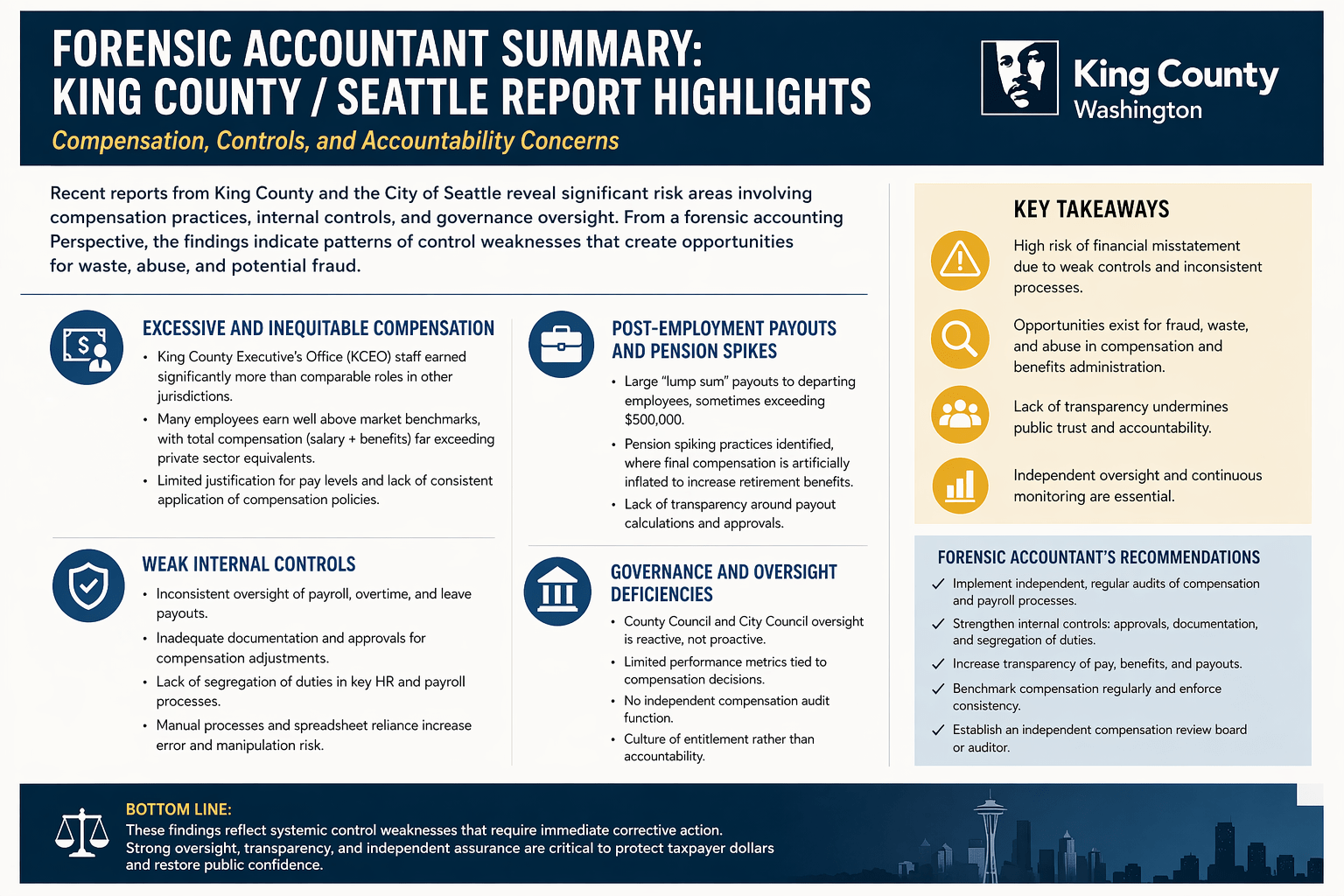

Breaking Down the Numbers: A Forensic Accountant’s View of the King County / Seattle Audit Findings

The visual summary tells a story that forensic accountants recognize immediately—not as a collection of isolated issues, but as a pattern. When you step back and connect the findings, what emerges is not just mismanagement, but systemic control failure across financial reporting, governance, and operational execution.

At the center of this analysis is the King County Regional Homelessness Authority (KCRHA), where a third-party forensic audit identified approximately $13 million that cannot be properly accounted for. From a forensic accounting perspective, that number alone is not the most concerning element. It is what makes up that number—and how it went undetected—that raises serious red flags.

The breakdown includes $8 million in unreconciled receivables, $4.26 million in administrative overspending, and $1.26 million tied to interest discrepancies. These are not minor bookkeeping issues. They represent failures in basic accounting disciplines: reconciliation, classification, and oversight.

Unreconciled receivables, in particular, signal a breakdown in one of the most fundamental accounting controls—knowing what is owed, what is collectible, and what is real. When leadership cannot clearly identify whether millions are valid or recoverable, it points to incomplete records or a lack of verification processes. In forensic terms, this creates a blind spot where both error and manipulation can occur.

The visual highlights weak internal controls, and the underlying findings reinforce that conclusion. There were consistent delays in invoicing—some stretching as long as 16 months. More than half of invoices submitted were delayed beyond standard timeframes. These delays do more than slow cash flow—they eliminate management’s ability to accurately forecast, monitor, and respond. When financial data is stale, decision-making becomes guesswork.

Compounding the issue is the recurring negative cash position, reaching tens of millions of dollars. That level of deficit is not simply a liquidity issue; it reflects structural problems in how funds are managed and disbursed. While explanations point to reimbursement timing and advance funding structures, those conditions should have been supported by controls designed to monitor and correct imbalances in real time.

From a forensic standpoint, cash flow misalignment without proper oversight is one of the most common environments where financial abuse can occur. It creates confusion, reduces accountability, and makes it significantly harder to trace the movement of funds.

The visual also emphasizes governance and oversight deficiencies—and again, the findings support this. Leadership turnover, delayed payments, unverified accounts, and inconsistent financial processes all contributed to the environment. These are not independent issues; they are symptoms of an organization that scaled without establishing a stable financial infrastructure.

One of the most telling concerns is the lack of proper tracking for significant infusions of public funds. In forensic accounting, any time large inflows are not clearly tracked and reconciled, the risk profile increases dramatically. It becomes difficult to determine whether funds were used as intended, misallocated, or simply lost in poor recordkeeping.

The infographic’s focus on accountability is well placed. What we see here is not just a failure of accounting—it is a failure of governance. When oversight bodies react after the fact rather than proactively monitoring financial health, systemic issues have time to take hold.

This situation reinforces a broader principle: rapid growth without parallel investment in controls is inherently risky. The agency was created to address a complex and urgent issue, but complexity does not reduce the need for financial discipline—it amplifies it.

The recommendations highlighted in the visual—independent audits, stronger internal controls, and improved transparency—are not optional safeguards. They are essential. But equally important is how they are applied. Scheduled audits provide structure, but unannounced audits reveal whether controls are actually functioning in day-to-day operations.

Ultimately, these findings reinforce a core forensic truth: financial failures rarely begin with fraud. They begin with weak controls, inconsistent processes, and lack of oversight. Left unaddressed, those conditions create the opportunity for larger failures—whether through error, waste, or intentional misuse.

The numbers are significant. But the real takeaway is structural. Without immediate and sustained improvements in financial governance, the risk is not just continued mismanagement—it is the erosion of public trust.

And once that trust is lost, it is far more difficult to restore than any balance sheet.